“Save your money and invest in something that will help you retire!” ” In the end, only land, animals, and water will matter… Get you some land!” “You can’t rely on the government for your retirement; you must invest in your retirement.” ” When you get to my age, you’re gonna wish you had saved your money!” If we could get $100 every time an older person told us this… We still wouldn’t be rich, which is sad because, today, it’s rare to find someone in their “golden years” who has saved enough to have a splendid retirement. For as long as we can remember, we have been told that the government would provide elderly care through Social Security. Provided that the taxpayer’s dollars would find their way to the Social Security fund. However, as the years scurried, we lost more and more of that “promised care.”

This led to us doing our own investing and self-funded retirement; even though investing and saving this money seems more and more daunting, it’s necessary for the very survival of our future. Investing is essential for securing your financial future and ensuring your wealth grows. By diversifying your investment portfolio with Traditional IRAs, Roth IRAs, 401(k)s, Certificates of Deposit (CDs), stocks, and precious metals like gold, silver, and rare coins, you can create a robust strategy to protect and enhance your wealth. Setting yourself up for your future retirement is essential and critical. The results of COVID-19 showed us that we as a Country are not ready, nor have we saved for our legacies or our retirement.

Navigating your future finances is very scary as the cost-of-living increases with time and the way the economy shifts without notice. It’s easy to find yourself looking for ways to secure your future and generate continuous cash flow streams. Whether it’s investing in ways that gain interest over the years, whether it’s a short return from the stock market, or selling your precious metals to help fund your livelihood, it’s always good to know your options and to know all the choices you have to make the best decision on how to invest your money. So, let’s get ready to pretend like you work at Charles Swab, Edward Jones, or Black Rock. We will break down the infrastructure of each form of investing, magnify the pros and cons of each, and ultimately help you see that you, too, can invest without having a Trillion dollars to spare.

In this blog, we’ll explore how each investment vehicle works and how they can generate continuous growth and be passed down to your children as an inheritance. We will understand why investing is much better than saving money and why leaving something for the next generation is essential. So, let’s get the current edition of the WSJ and the NY Times. Grab a copy of the Rob Report and the latest edition of The Economist, and we will join the wolves of Wall Street to understand your financial options to become an investing warrior!!

Traditional and ROTH IRAs

The History of the IRA

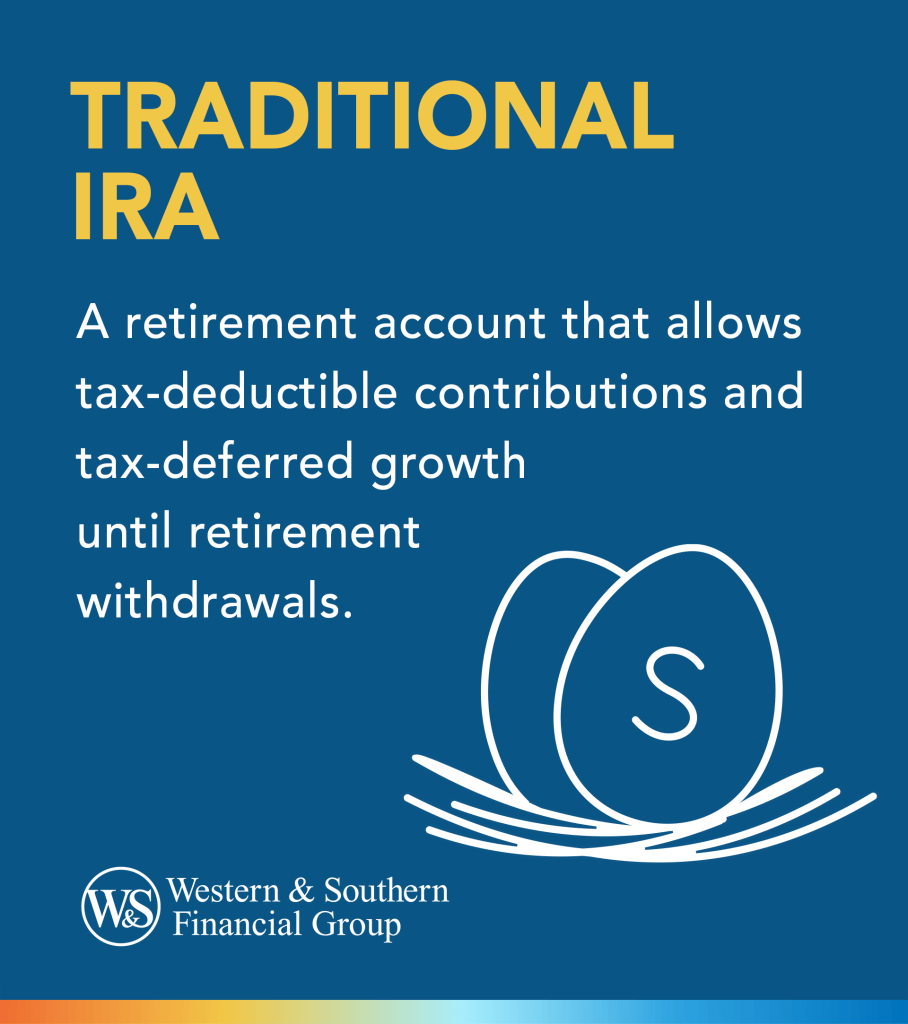

The Traditional Individual Retirement Account (IRA) was part of the Employee Retirement Income Security Act of 1974 (ERISA), spearheaded by the United States Congress. This pioneering move was designed to encourage Americans to save for retirement by offering tax advantages as an incentive. The Traditional IRA allows individuals to make pre-tax contributions, meaning the contributions may be tax-deductible depending on the individual’s income, filing status, and other factors. Taxes are then paid on the withdrawals during retirement, ideally at a lower tax rate due to the individual’s reduced income. The creation of the Traditional IRA marked a significant shift towards empowering individuals to take control of their retirement savings, moving away from reliance on employer-sponsored pension plans.

The Roth IRA, introduced in 1997 through the Taxpayer Relief Act, was named after Senator William Roth of Delaware, a major proponent of the legislation. Unlike its predecessor, the Roth IRA was designed with after-tax contributions in mind, meaning that individuals pay taxes on the money they contribute upfront. However, the significant advantage of the Roth IRA is that both the contributions and the earnings can be withdrawn tax-free in retirement, provided certain conditions are met. This innovative approach was created to offer a flexible savings option that would adapt to different financial situations and planning strategies, allowing for tax-free growth and distribution. The introduction of the Roth IRA represented an evolution in retirement saving, catering to the changing needs of Americans and encouraging a more proactive and diversified approach to retirement planning.

Traditional IRA

A Traditional Individual Retirement Account (IRA) is a retirement savings account that allows individuals to save for retirement on a tax-deferred basis. This means that contributions to a Traditional IRA may be tax-deductible in the year they are made, depending on the taxpayer’s income, filing status, and other factors. Still, taxes are paid on withdrawals during retirement. The main goal of a Traditional IRA is to provide financial security in retirement, allowing savings to grow tax-deferred until they are withdrawn in retirement years, typically when the individual may be in a lower tax bracket.

Traditional IRAs are funded through individual contributions. For the tax year 2023, the maximum contribution limit is $6,000 for individuals under 50 and $7,000 for those 50 and older, which accounts for a catch-up contribution. These contributions can be made in cash or checks or by transferring assets from another retirement account. The funding of a Traditional IRA does not directly involve the individual’s employer, unlike 401(k) plans or other employer-sponsored retirement plans.

However, some employers offer Simplified Employee Pension (SEP) IRAs or Savings Incentive Match Plan for Employees (SIMPLE) IRAs, which are types of Traditional IRAs that involve employer contributions. In these plans, the employer may match a percentage of the employee’s contributions up to a specific limit, enhancing the employee’s retirement savings. This differs from a 401(k) plan, where employer matching is more commonly associated. In the context of a Traditional IRA, matching contributions primarily apply to SEP and SIMPLE IRAs rather than individual Traditional IRAs.

When changing jobs, your Traditional IRA remains unaffected since it is an independent account of your employer. This portability is a significant advantage of Traditional IRAs over employer-sponsored plans like 401(k)s. Suppose you have an employer-sponsored plan from a previous job, such as a 401(k). In that case, you can roll these funds into a Traditional IRA without incurring taxes or penalties, preserving the tax-deferred status of your retirement savings. This rollover process allows individuals to consolidate their retirement accounts, making it easier to manage their investments and access a broader range of investment options than those offered by employer plans.

ROTH IRA

A Roth Individual Retirement Account (Roth IRA) is a retirement savings account offering tax-free growth and tax-free retirement withdrawals under certain conditions. Unlike traditional IRAs, where contributions may be tax deductible, but withdrawals are taxed, contributions to a Roth IRA are made with after-tax dollars. The withdrawals are tax-free if the account has been open for at least five years and the holder is at least fifty-nine and a half years old.

Usage and Fund Transfer: The funds in a Roth IRA can be invested in various assets such as stocks, bonds, mutual funds, and ETFs, allowing the account holder to grow their retirement savings tax-free potentially. Contributions can be withdrawn anytime without taxes or penalties, making the Roth IRA a retirement vehicle and a flexible savings account. However, there are limits to how much you can contribute each year, and eligibility to contribute phases out at higher income levels.

Portability Across Jobs: One of the critical features of a Roth IRA is its portability; it is not tied to your employer like a 401(k) or other employer-sponsored retirement plans. This means you can maintain your Roth IRA and continue contributing to it as you move from job to job. This continuity is a significant advantage for workers who change employers frequently or work in industries with high turnover rates.

Employer Match and Roth IRA: Unlike 401(k) plans, employers do not match contributions to individual Roth IRAs. Employer matches are typically associated with employer-sponsored retirement plans. However, some employers offer a Roth option within their 401(k) plans, where they might match contributions, but this is separate from an individual Roth IRA.

Advantages Over Traditional IRA: The Roth IRA may be better than a traditional IRA for several reasons, depending on your tax situation and retirement planning goals. Since Roth IRA withdrawals in retirement are tax-free, they can be particularly advantageous for individuals who expect to be in a higher tax bracket in retirement than they are now. This makes the Roth IRA an excellent tool for tax diversification in retirement planning. Additionally, the Roth IRA does not require distributions based on age, unlike a traditional IRA, which requires minimum distributions starting at age 72. This feature allows for more flexible retirement planning and the potential for tax-free wealth transfer to heirs.

401(K)

The 401(k) plan, a cornerstone of American retirement planning, was initially designed for something other than its current purpose. It emerged from the Revenue Act of 1978, and its potential for retirement savings was popularized in the early 1980s, thanks to the efforts of benefits consultant Ted Benna. Benna noticed that the tax code, specifically section 401(k), could be used to create a tax-advantaged retirement savings plan for employees. This realization led to the first 401(k) plans being offered by employers in 1981. The intention behind the 401(k) was to complement traditional pension plans and give employees a tax-efficient way to save for retirement.

The workings of a 401(k) are straightforward. Employees elect to have a portion of their salary deferred into the plan, which is then invested in a selection of mutual funds, stocks, bonds, or other assets. These contributions are typically made pre-tax, which can lower the employee’s taxable income. Taxes on contributions and earnings are deferred until the money is withdrawn, usually after retirement. Many employers also contribute to their employees’ 401(k) plans, often matching contributions to a certain percentage, which can significantly enhance retirement savings growth.

One of the critical features of a 401(k) plan is its portability. When changing jobs, an employee can roll over their 401(k) into the new employer’s plan without penalty, or they can opt to roll it into an Individual Retirement Account (IRA). This flexibility allows for continuous retirement savings growth, regardless of career moves.

Choosing between a 401(k), an IRA, or direct investment in stocks depends on an individual’s financial situation, tax considerations, and retirement goals. A 401(k) may offer higher contribution limits and employer matching, making it an attractive option for those with access to a generous plan. On the other hand, IRAs provide more investment options and may be preferable for those looking for more control over their retirement savings. Direct investing in stocks suits individuals seeking higher returns and those comfortable with higher risks.

Certificates of Deposits (CDs)

Certificates of Deposit (CDs) are a financial instrument that originated for banks to raise funds by borrowing money from their customers for a fixed period. The concept has existed since the early 1960s in the United States, evolving from the traditional savings accounts that offered a way to save money with interest. CDs were created as a mutually beneficial product; they provided banks with a stable source of funds locked in for a predetermined period, and in return, depositors were offered a higher interest rate than regular savings accounts. This arrangement allowed banks to better manage their liquidity and lending capabilities while providing customers with a low-risk investment option with a guaranteed return.

The key attraction of CDs lies in their safety and predictability. They work with a depositor agreeing to lend money to the bank for a fixed term, ranging from a few months to several years. In return, the bank pays interest on that amount at a fixed rate, higher than a standard savings account. The interest rate is determined at the start, allowing depositors to calculate their exact earnings at the end of the term. This fixed interest rate and term protect depositors from interest rate fluctuations that can affect other savings and investment products. Furthermore, the Federal Deposit Insurance Corporation (FDIC) typically insures CDs up to certain limits, providing an additional layer of security for the investment.

For individuals looking for a stable, low-risk investment, CDs may be more appealing than IRAs, precious metals, 401(k)s, and stocks due to their predictability and safety. Unlike stocks and precious metals, which can be volatile and subject to market fluctuations, CDs offer a guaranteed return, making them a safer choice for conservative investors or those nearing retirement who cannot afford to risk their principal. While IRAs and 401(k)s offer tax advantages and potentially higher returns through investment in the stock market or other securities, they also come with higher risk and less liquidity. CDs, on the other hand, provide a fixed, predictable return and are easily accessible at the end of the term, making them an excellent choice for investors looking for a short-term, secure place to park their money or for those seeking to diversify their investment portfolio with a low-risk option.

Stocks

The concept of stocks and stock markets dates to the 1600s, with the Amsterdam Stock Exchange often considered the world’s first. Stocks were created as a means for companies to raise capital without having to take on debt. By selling ownership shares to investors, companies could fund expansion, pay off debt, or finance new ventures. This method of raising funds was revolutionary because it spread the financial risk among a vast pool of shareholders rather than concentrating it on a single entity or group of lenders. As commerce and industry expanded, the need for such a financial mechanism became increasingly vital, facilitating the growth of companies and, by extension, economies at large.

Stocks work by representing a share of ownership in a company. When an investor buys a company’s stock, they effectively purchase a small part of that company. As the company grows and becomes more profitable, the value of its stock is likely to increase, thereby increasing the wealth of its shareholders. Moreover, investors may receive dividends, portions of a company’s earnings distributed to shareholders. The stock market is a complex ecosystem where stocks are bought and sold, with prices determined by supply and demand dynamics. This system allows for liquidity, meaning investors can readily buy or sell stocks, and provides a mechanism for price discovery, reflecting companies’ perceived value and prospects.

When comparing stocks to other investment vehicles like IRAs, precious metals, 401(k)s, and Certificates of Deposit (CDs), stocks often offer the potential for higher returns, albeit with higher risk. Unlike the stable but lower returns of CDs or the tax-advantaged growth of IRAs and 401(k)s, stocks can provide substantial capital appreciation over time. This makes them an attractive option for long-term investors willing to weather market volatility in pursuit of greater rewards. Furthermore, while precious metals like gold can hedge against inflation or economic downturns, they do not produce income or dividends. Stocks, therefore, offer a unique combination of growth potential and income through dividends, making them a compelling choice for investors seeking to build wealth over time.

Gold, Silver, and Precious Metals

Investing in gold, silver, and rare coins has long been a popular choice for many investors seeking diversification outside traditional investment vehicles like IRAs, stocks, 401(k)s, and certificates of deposit. These tangible assets offer a unique blend of historical significance, inherent value, and a physical hedge against inflation and currency devaluation. The allure of precious metals and collectible coins lies in their scarcity and demand, which can drive up value independently of stock market performance. Moreover, gold and silver are often viewed as “haven” assets during economic uncertainty, as their prices typically move inversely to stock market trends, providing a buffer for investment portfolios during downturns.

However, investing in precious metals and rare coins comes with its own set of challenges and considerations. The market for these items can be volatile, with prices fluctuating due to geopolitical events, currency values, and changes in supply and demand. Unlike stocks or bonds, gold, silver, and rare coins do not generate income through dividends or interest, meaning their investment return depends entirely on capital appreciation. Additionally, there are costs associated with the physical storage and insurance of these assets, and the market for rare coins requires a level of expertise to navigate successfully, as the value can be significantly influenced by rarity, condition, and historical significance.

The connection between the prices of precious metals and the stock market is complex, often reflecting broader economic sentiments rather than direct stock market performance. During a stock market decline or economic recession, investors may flock to gold and silver as a protective measure, which can drive up prices. This inverse relationship makes them an appealing choice for investors looking to hedge against stock market volatility. Compared to traditional retirement accounts and savings options like IRAs, 401(k)s, and CDs, which are tied to the performance of financial markets and interest rates, gold, silver, and rare coins can offer a non-correlated asset class that enhances portfolio diversification. This diversification can help manage risk and provide better protection against inflation and economic shifts, making them a valuable addition for investors seeking to safeguard their wealth over the long term.

Passing on Investments as Inheritance

When planning to pass on investments such as Roth and Traditional IRAs, stocks, certificates of deposit (CDs), and 401(k)s as inheritance, it’s crucial to understand the rules and strategies that govern each type of investment to ensure they are successfully transferred to your beneficiaries without unnecessary government confiscation or heavy tax penalties. The key for Roth and Traditional IRAs is to designate beneficiaries directly through the account paperwork. This designation allows these assets to pass directly to the named individuals outside the probate process. Roth IRAs are particularly advantageous for heirs because withdrawals are tax-free. However, it’s important to note that beneficiaries may need to take required minimum distributions (RMDs), depending on their relationship to the deceased and the account type, with different tax implications for inherited Traditional IRAs.

Similar beneficiary designation principles apply to stocks, certificates of deposit, and 401(k)s. By naming beneficiaries directly on these accounts, you can ensure a smoother transfer of assets upon your death. Stocks and CDs held in taxable accounts can also receive a “step-up” basis, meaning the value of these assets is recalculated at the time of the owner’s death, potentially reducing capital gains taxes if the beneficiary decides to sell. For 401(k)s, beneficiaries must understand their options, including rolling the account into an Inherited IRA to stretch out distributions and tax payments over time. However, the rules can vary depending on the relationship between the deceased and the plan’s specifics.

To prevent these assets from being unnecessarily confiscated by the government or eroded by taxes, careful planning and regular review of your estate plan are essential. This includes keeping beneficiary designations up to date and considering the creation of trusts in some cases, which can offer more control over the distribution of assets and protection from creditors. Consultation with a financial advisor or estate planning attorney can provide personalized advice tailored to your situation, helping you navigate inheritance and taxation’s complex rules. It’s also vital to educate your beneficiaries on their options and the tax implications of their inherited assets, ensuring they make informed decisions that align with their financial goals and the original intent of the inheritance.

One of the critical aspects of wealth management is ensuring that your wealth is passed down to future generations. Each of these investment vehicles has specific considerations for inheritance:

- IRAs and 401(k)s: Beneficiaries must be designated for these accounts. They can be inherited, but the rules for distributions can vary, especially after recent changes in legislation.

- CDs and Stocks: These can be bequeathed through your will or by setting up transfer-on-death (TOD) arrangements, allowing them to pass directly to your beneficiaries without going through probate.

- Precious Metals and Coins: As physical assets, they can be left to heirs in a will or trust, offering a straightforward transfer of wealth.

Final Thoughts

No matter what you choose, it’s just a wonderful thing that you chose in the first place. If you are still on the fence about investing, I suggest you seek financial guidance or speak with a licensed investor for a consultation. Diversifying your investment portfolio across Traditional IRAs, Roth IRAs, 401(k)s, CDs, stocks, and precious metals can provide a balanced approach to growing wealth. Each option offers different benefits, from tax advantages to protection against inflation. When choosing the right mix, consider your risk tolerance, investment horizon, and retirement goals. Also, proper estate planning ensures that these investments benefit your family. Consulting with financial and legal professionals can provide tailored advice for your unique situation.

A Traditional IRA offers a tax-advantaged way to save for retirement, funded by individual contributions that may be tax-deductible. While it doesn’t involve direct employer matching like a 401(k) plan, certain employer-sponsored IRAs can offer similar benefits. The ability to roll over funds from employer-sponsored plans to a Traditional IRA without tax penalties provides flexibility and continuity in retirement planning, regardless of job changes. A Roth IRA offers a flexible, portable retirement savings option with the benefits of tax-free growth and withdrawals. Its advantages over traditional IRAs make it an attractive choice for many individuals, especially those who anticipate higher retirement taxes or value the flexibility of penalty-free access to contributions.

The best choice varies by individual circumstances. For those with access to a 401(k) with employer matching, contributing enough to get the full match is often recommended as it represents an immediate, risk-free return on investment. Beyond that, diversifying retirement savings with IRAs or direct stock investments can provide additional flexibility and potential for growth. Consulting with a financial advisor can help determine the most appropriate strategy based on individual goals, risk tolerance, and financial situation.